1. According to the SMM survey, coke profit per mt was -2.9 yuan/mt this week, with most coke enterprises starting to incur losses.

From a pricing perspective, coke prices underwent the tenth round of price cuts this week, with a reduction of 50-55 yuan/mt, further negatively impacting coke profit per mt. From a cost perspective, coal mines maintained normal production, and coking coal supply remained at a high level. However, after a prolonged and continuous decline, the downward space for coking coal prices is limited, and the price reduction is slow, making it difficult to restore coke enterprises' profitability.

Coke prices are not expected to decline next week, while some types of coking coal may see supplementary price reductions, leading to a slight decrease in coking costs. Coke profit per mt is expected to remain near the break-even point.

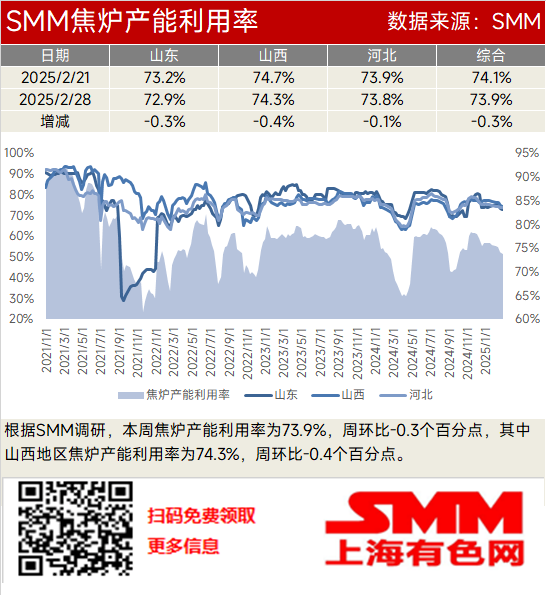

2. According to the SMM survey, the coke oven capacity utilisation rate was 73.9% this week, down 0.3 percentage points WoW. In Shanxi, the coke oven capacity utilisation rate was 74.3%, down 0.4 percentage points WoW.

From a profitability perspective, most coke enterprises experienced losses, but these were generally minor and had little impact on production. From an inventory perspective, coke enterprises still faced significant shipment pressure, with overall coke inventory remaining at a high level, suppressing production enthusiasm. From an environmental protection perspective, environmental protection policies in Shanxi, Hebei, and Shandong were not tightened, having no significant impact on coke production.

Most coke enterprises are expected to remain near the break-even point, within a tolerable range for most, with only a small number reducing production. Coke supply remains ample. However, the end-use market recovery has been slow, falling short of expectations, and coke inventory at steel mills remains at safe levels, with steel mills primarily purchasing as needed. In summary, the ample coke supply situation is unlikely to change in the short term. Additionally, losses at some coke enterprises suppress production enthusiasm, and the coke oven capacity utilisation rate at coke enterprises is expected to decline slightly next week.

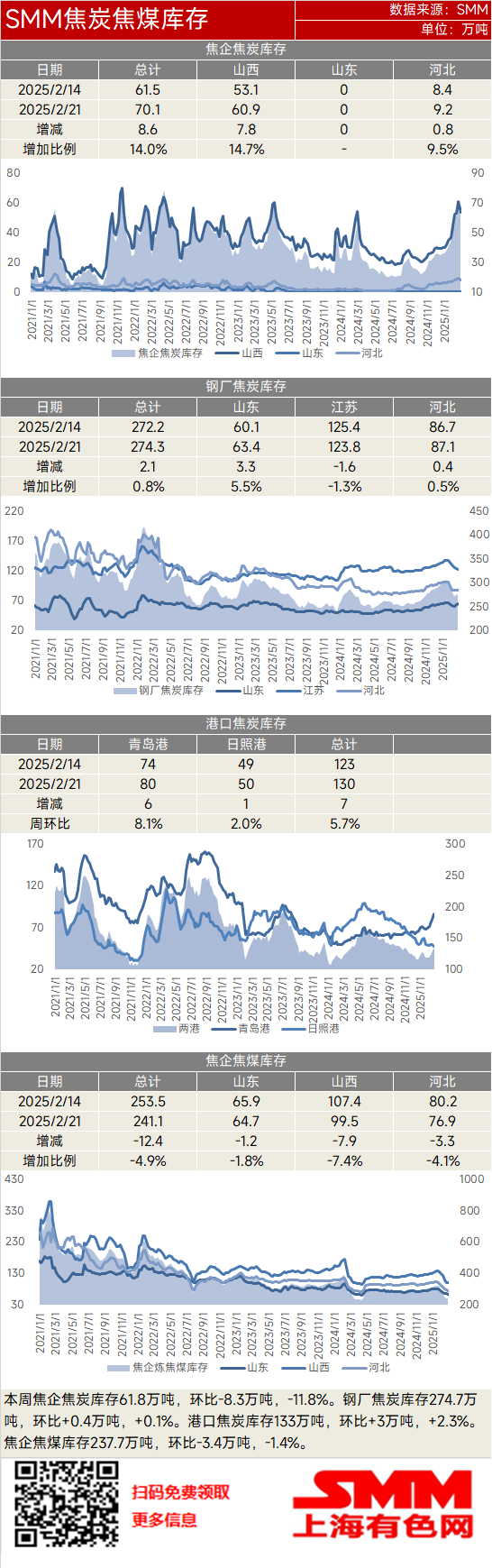

3. This week, coke inventory at coke enterprises was 618,000 mt, down 83,000 mt (-11.8%) WoW. Coke inventory at steel mills was 2.747 million mt, up 4,000 mt (+0.1%) WoW. Coke inventory at ports was 1.33 million mt, up 30,000 mt (+2.3%) WoW. Coking coal inventory at coke enterprises was 2.377 million mt, down 34,000 mt (-1.4%) WoW.

This week, coke inventory at coke enterprises began to decline, while coke inventory at steel mills fluctuated rangebound. Most coke enterprises started to incur minor losses, with some reducing production enthusiasm, leading to a tightening of coke supply and a gradual decline in coke inventory at coke enterprises. The steel market underperformed expectations this week, with pig iron production at steel mills continuing to decline slightly, reducing daily coke consumption. Additionally, on February 27, Trump imposed additional tariffs, affecting market confidence, and steel mills primarily purchased coke as needed.

Subsequently, production at most coke enterprises may decline slightly, tightening coke supply. However, demand from the end-use market at steel mills remains moderate, and their coke inventory is at safe levels. Even with the anticipated positive policies from the Two Sessions, steel mills are expected to continue purchasing as needed. Therefore, coke enterprises are expected to shift to destocking next week, while coke inventory at steel mills is likely to fluctuate rangebound.

This week, coke supply began to tighten, with limited room for cost reductions. Coupled with traders' expectations for policies from the Two Sessions, they slightly restocked inventories, and coke inventory at ports is expected to increase next week.

This week, coking coal inventory at coke enterprises continued to decline, but the rate of decline narrowed. The main reason is that after a prolonged and continuous decline in coking coal prices, the downward space is limited, and price reductions are slow. Even though downstream acceptance of current coking coal prices remains low, it is difficult for coking coal prices to decline significantly again. Some coke enterprises have started purchasing. Subsequently, coking coal prices are expected to have hit bottom, and some coke enterprises with restocking needs may begin actively purchasing. Coking coal inventory at coke enterprises is expected to stop declining next week.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)